Planning how to use your retirement budget and pass assets down to beneficiaries often comes with a steep learning curve, making estate taxes easy to overlook. Estate taxes, sometimes referred to as a death tax, are paid by your estate before any assets are distributed to heirs. While high exemption limits mean most properties aren’t subject to federal estate taxes, states with estate taxes have much lower thresholds.

Estate taxes apply to everything you own at the time of your passing and can have a significant impact on the assets you plan to pass to family members. Learning which states levy estate taxes and how estate taxes work can help you prepare for your spending during retirement and your family’s future.

What Is an Estate Tax?

An estate tax is a tax levied on the transfer of assets at death. States with estate taxes set their own exemption limits, and the amount owed is a percentage of the value of the deceased’s estate.

Estate taxes apply to your gross estate, which is everything you own, including:

- Real estate (primary and vacation homes)

- Retirement accounts (IRAs 401k(s), Roth accounts)

- Business interests

- Personal property

- Cash and bank accounts

- Investment portfolios

- Life insurance proceeds (in certain situations)

Federal vs. State Estate Taxes

Federal estate taxes have a high exemption threshold, so they apply only to large estates. Beginning in 2026, the federal estate tax exemption is set at $15 million per individual, and $30 million for married couples. State estate taxes are levied at the state level, and may apply at much lower thresholds.

Estate Tax vs. Inheritance Tax

It’s important to note that estate taxes and inheritance taxes are not the same thing. An estate tax is levied against your estate before your assets are transferred to your beneficiaries. It’s based on the total value of your estate, including all assets. An inheritance tax is levied against your beneficiaries, based on their relationship to you and the amount they inherited.

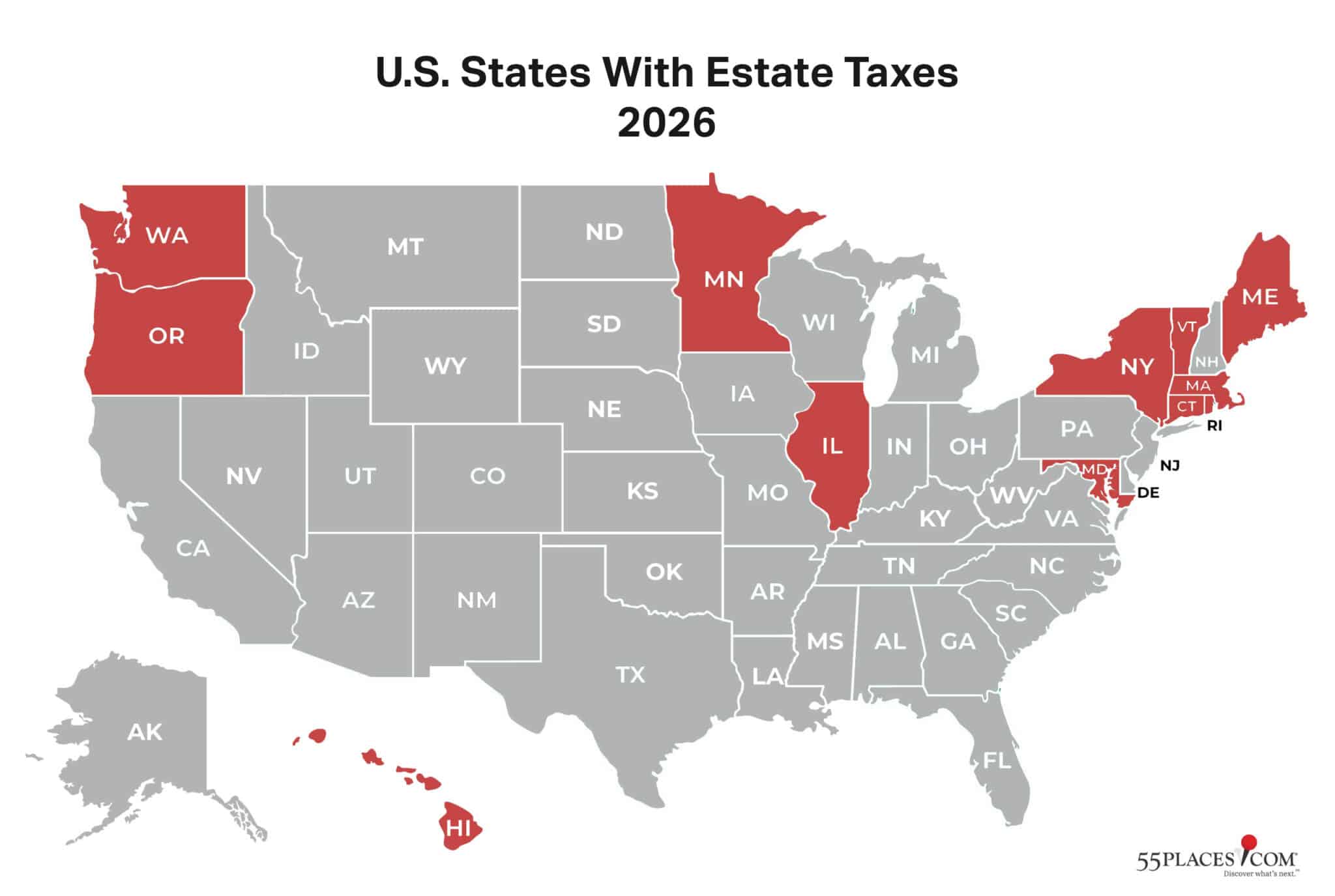

Which States Have Estate Taxes in 2026?

Not every state imposes estate taxes. Currently, only 12 states and the District of Columbia levy estate taxes at the state level. However, laws can change, so it’s essential to verify current thresholds when beginning or updating your estate planning process.

States with state estate taxes in 2026 include:

- Connecticut: Exemption amount is equal to that of federal state taxes (currently $15 million), with a flat tax rate of 12%

- Hawai‘i: Exemption amount is $5.49 million, with tax rates ranging from 10% – 20%

- Illinois: Exemption amount is $4 million, with tax rates ranging from 0.8% – 16%.

- Maine: Exemption amount is $7.16 million, with tax rates set at 8%, 10%, or 12%

- Maryland: Exemption amount is $5 million, with tax rates ranging from 0.8% – 16%

- Massachusetts: Exemption amount is $2 million, with tax rates ranging from 0.8% – 16%

- Minnesota: Exemption amount is $3 million, with tax rates ranging from 13% – 16%

- New York: Exemption amount is $7.35 million, with tax rates ranging from 3.06% – 16% — New York also has an “estate tax cliff” that imposes tax on an entire estate when the value of a taxable estate exceeds 105% of the exemption amount ($7,717,500 for 2026).

- Oregon: Exemption amount is $1 million (the lowest exemption in the nation), with tax rates ranging from 10% to 16%

- Rhode Island: Exemption rate is $1,838,056 and adjusted annually for inflation, with tax rates ranging from 0.8% – 16%

- Vermont: Exemption rate $5 million, with a flat tax rate of 16%

- Washington: Exemption rate is currently $3.076 million (falling to 3 million on July 1, 2026), with tax rates ranging from 10% – 35% (will be 10% – 20% beginning July 1, 2026)

- District of Columbia: Exemption amount is $4,988,400, with tax rates ranging from 11.2% – 16%.

States With Both Estate and Inheritance Taxes

Only five states impose an inheritance tax, including Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

Maryland is the only state with both an estate and an inheritance tax. The inheritance tax is assessed at 10% on heirs who inherit property valued at more than $1,000. Maryland’s inheritance tax doesn’t apply if the heir is the spouse, parent, stepparent, grandparent, child, stepchild, grandchild (or other lineal descendant of a child), sibling, son-in-law, daughter-in-law, or surviving spouse of a deceased child who hasn’t remarried.

How Much Are State Estate Taxes?

The cost of estate taxes varies by location and estate value. States with estate taxes set a specific exemption amount and a percentage rate at which assets are taxed. As with federal tax, state estate taxes only apply to the portion of the estate that surpasses the exemption amount.

Exemption Thresholds Vary Widely

Since each state sets its own exemption rate, estates subject to taxation can vary significantly. Some states have exemption rates set at $1 million, while others have much higher thresholds, tied to inflation. Oregon has the lowest exemption amount at $1 million, while Connecticut has the highest, at $15 millon.

Tax Rates Differ by State

As with exemption amounts, tax rates (the percentage at which your assets are taxed) vary. Percentage rates may be a flat rate for all applicable estates or range based on the estate’s value. Rates in many jurisdictions are progressive, with the highest taxation rates exceeding 15%.

Why Location Matters

A home, business, or investment property in a taxable state can significantly affect estate planning. Regardless of the beneficiary’s location, estate taxes are applied based on the estate’s location.

How to Reduce or Plan for Estate Taxes

Careful estate planning can help you reduce estate taxes or plan for how they’ll be paid. There are several options property owners can consider to reduce tax burdens for beneficiaries.

Use Trusts

Trusts are financial vehicles used to help you assign assets to your beneficiaries before you pass. It is an arrangement in which you transfer your home into a trust in your name, list your beneficiaries as heirs, and allow you to continue to use the property as your primary residence. While a revocable trust allows you to make changes during your lifetime, an irrevocable trust (that cannot be changed) removes assets from your estate, reducing its value. This could make you eligible for reduced estate taxes or a full exemption, depending on your circumstances.

Lifetime Gifting Strategies

Annual gifts can reduce your estate’s size, reducing state tax burdens or making you eligible for an exemption. In 2026, you can give any number of people up to $19,000 each year without incurring a taxable gift. The recipient typically owes no taxes, allowing you to distribute your assets during your lifetime.

Relocation Considerations

If you’re seeking a retirement home, considering a state without estate taxes can completely remove the burden. Whether you’re downsizing or maintaining ownership of your current property, assets in a state without estate taxes won’t be included in the taxable amount elsewhere.

Keep Beneficiary Designations Updated

Having beneficiaries named on relevant accounts is the smoothest way to transfer assets. Coordinate wills, trusts, retirement accounts, and insurance policies to ensure assets are distributed as intended. Financial institutions follow names on file, even if they conflict with wills and trusts.

Work with Professionals

People often make the mistake of assuming estate planning is only for the wealthy. When state estate taxes have exemptions as low as $1 million, all individuals should be aware that inheritance can be substantially reduced by taxes. However, estate planning can be complex. By working with professionals, such as an estate attorney, CPA, or financial advisor, you can make informed decisions about your retirement budget and how to distribute your assets.

FAQ: Estate Taxes

Which states have estate taxes in 2026?

Twelve states and the District of Columbia levy estate taxes: Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, and the District of Columbia.

What is the difference between an estate tax and an inheritance tax?

An estate tax is levied against the total value of your estate before assets are distributed to heirs. An inheritance tax is levied on beneficiaries based on their relationship to the deceased and the amount they inherit.

What is the federal estate tax exemption in 2026?

The federal estate tax exemption is $15 million per individual and $30 million for married couples beginning in 2026. Only estates valued above those thresholds are subject to the federal estate tax.

Which state has the lowest estate tax exemption?

Oregon has the lowest estate tax exemption in the nation at $1 million, with tax rates ranging from 10% to 16%. This means any Oregon estate valued above $1 million is subject to state estate taxes on the amount exceeding the threshold.

Which state has the highest estate tax exemption?

Connecticut has the highest state estate tax exemption at $15 million, matching the federal exemption. Connecticut applies a flat 12% tax rate on the portion exceeding the threshold.

Does estate tax location depend on where I live or where my property is?

Estate taxes are applied based on where the assets are located, not where the beneficiary lives. If you own a home, business, or investment property in a state with an estate tax, those assets may be subject to that state’s tax regardless of your primary residence. This is an important consideration for retirees who own property in multiple states.

How can I reduce estate taxes?

Several strategies can reduce estate taxes. Irrevocable trusts remove assets from your estate, potentially lowering its value below the exemption threshold. Annual gifting allows you to give up to $19,000 per person in 2026 without incurring a taxable gift. Relocating to a state without estate taxes eliminates the burden entirely. Keeping beneficiary designations up to date on retirement accounts, insurance policies, and other financial accounts ensures smooth asset transfers. Working with an estate attorney or financial advisor is recommended.

What is an irrevocable trust?

An irrevocable trust is a financial arrangement where you transfer assets into a trust that cannot be changed once established. Because the assets are no longer considered part of your estate, they reduce its total value, potentially making you eligible for reduced estate taxes or a full exemption. A revocable trust allows changes during your lifetime but does not remove assets from your estate for tax purposes.

How much can you gift per year without paying estate taxes?

In 2026, you can gift up to $19,000 per person per year without incurring a taxable gift. There’s no limit on the number of people you can gift to. The recipient typically owes no taxes on the gift. Annual gifting is a common strategy for reducing your estate’s total value over time, potentially lowering or eliminating state estate tax exposure.

Which states have both estate and inheritance taxes?

Maryland is the only state with both an estate tax and an inheritance tax. Maryland’s estate tax exemption is $5 million, with rates from 0.8% to 16%. Its inheritance tax is 10% on property valued at over $1,000 that is inherited by non-exempt heirs.

Do most people pay estate taxes?

Most people do not pay federal estate taxes because the $15 million exemption ($30 million for married couples) excludes the vast majority of estates. However, state estate taxes have much lower thresholds. When you include real estate, retirement accounts, investments, life insurance proceeds, and other assets, more estates than expected can exceed state thresholds. An estimated awareness gap means many property owners don’t plan for state-level taxes until it’s too late.

Should retirees consider estate taxes when choosing where to retire?

Yes. If you’re choosing a retirement destination, moving to a state without estate taxes can completely eliminate the state-level burden on your heirs. Thirty-eight states have no estate tax. Even if you maintain property in a taxable state, assets located in a non-taxable state won’t be included in that state’s taxable amount. Estate tax exposure should be one factor alongside cost of living, climate, health care, and lifestyle when evaluating where to retire.

Do I need a professional for estate planning?

Working with an estate attorney, CPA, or financial advisor is strongly recommended. Estate planning involves trusts, beneficiary designations, gifting strategies, tax thresholds, and coordination across wills, retirement accounts, and insurance policies—all of which interact in complex ways. A professional can help you make informed decisions to protect your retirement budget and ensure your assets are distributed as intended.

- Insights and market stats

- Instant new home alerts

- Answers from local 55+ experts